Carbon Reduction

carbon-reduction

Climate Strategy

climate-strategy

7 min. read

Key takeaways

The UK's new biomass Contracts for Difference framework will cut industrial wood pellet imports by slightly more than half starting in April 2027. As a result, US producers will be left competing for only 1.6 million GST, an 80% reduction in US-addressable volume, with no successor market locked in.

Producers who move now to upgrade sustainability credentials and build relationships in emerging markets will be best positioned to capture the next generation of demand. Those who wait may find the most attractive offtake opportunities already structured around someone else's supply.

Four domestic markets now present producers with new demand opportunities: cofiring, sustainable aviation fuel (SAF), low-carbon steel, and bioenergy with carbon capture and storage (BECCS). Of these, BECCS for data centers is the strongest structural fit: hyperscalers need clean, firm power, pellet mills need offtakers, and the feedstock infrastructure is already in place.

The demand cliff is real, and the timeline is short

A pellet made in southern Mississippi this morning will be burned in a UK boiler about four weeks later. North America is on pace to ship more than 9 million green short tons (GST) of pellets to the UK each year—making the UK the world's largest consumer of wood pellets since 2018. The US Southeast is at the center of that supply chain: 28 large mills, 13.5 million GST of production capacity, rail spurs, export terminals, and bulk carriers, built almost entirely around UK demand.

However, the UK's new low-carbon Contracts for Difference (CfD) framework caps biomass power generators at a 27% annual capacity factor starting April 2027, down from roughly 64% today. When run hours fall by half, pellet demand follows. Existing subsidies expire in the first quarter of 2027, and the new CfD runs only to March 2031 with no commitment beyond that. Plant closures in Arkansas and Washington state, along with reduced output in Canada, are already early signals of supply chain contraction.

The math of who gets squeezed

The math is stark. By the second quarter of 2027, total annual UK pellet demand drops to 4.9 million GST. Of that:

Approximately 2.3 million GST goes to captive, integrated UK supply chains.

Approximately 1.0 million GST goes to Baltic suppliers, whose shipping times of one week or less become a decisive advantage as UK plants shift from baseload to dispatchable operation.

That leaves US producers competing for only 1.6 million GST. If Baltic suppliers capture more, US wood pellet exports to the UK could be effectively eliminated by 2031.

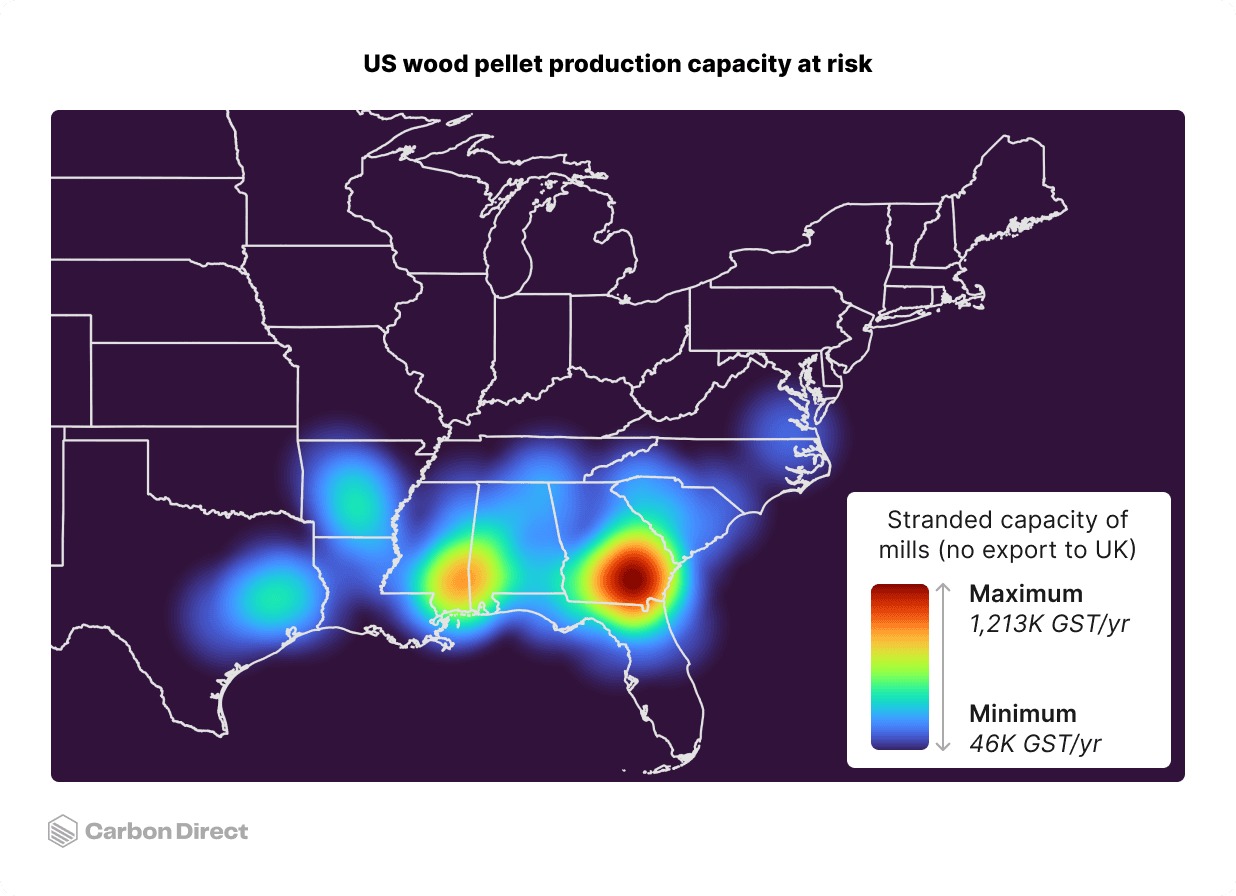

Figure 1. The US wood pellet production capacity is at risk of reduced demand from the UK starting in 2027. However, this production is well-positioned for alternative domestic uses.

Sustainability qualification is also tightening. The new CfD cuts the supply-chain emissions ceiling from 55.6 grams of carbon dioxide equivalent per megajoule (gCO₂e/MJ) to 36.6 gCO₂e/MJ. The framework assesses compliance mill by mill, not on a portfolio average. A cleaner mill cannot carry a dirtier sibling through the door.

The producers who understand this math now have roughly 18 months to position themselves for what comes next.

From stranded supply to new markets

The US Southeast's wood basket is robust: abundant inventory, strong growth-to-removal ratios, and more available residues than ever. The infrastructure is in place. The question is whether the next generation of markets can be developed quickly enough to redeploy this supply before the infrastructure sits idle.

Four pathways stand out as the strongest options for redeploying US pellet supply: bioenergy with carbon capture and storage (BECCS) for data centers, low-carbon steel, sustainable aviation fuel (SAF), and domestic cofiring. We have rigorously assessed the logistics economics, sustainability cases, and project development for each.

BECCS for data centers: The strongest structural fit

BECCS as a power source for data centers is the most compelling match for the situation pellet producers now face. The timing, feedstock requirements, and buyer characteristics align closely in a way that few other emerging markets can match.

Hyperscalers, the large data center operators driving an unprecedented surge in electricity demand, are signing deals for nuclear, geothermal, and small modular reactors alongside natural gas and renewables. They are doing this because annual Renewable Energy Certificates (RECs) are no longer sufficient to compensate for their scope 2 emissions, and they need clean, firm generation that can be matched to load on an hourly basis.

BECCS delivers exactly that. The Louisiana Green Fuels project—advanced by Strategic Biofuels and Carbon Direct—illustrates the model: regionally sourced forestry residues and sawmill waste generate 75 megawatts (MW) of firm electricity while sequestering over one million tonnes of CO₂ annually in deep saline formations. An ample supply of wood pellets creates a strategic opportunity for similar projects to move forward with certainty around feedstock processing, logistics, and costs.

The remaining commercial barrier is deal structure, not technology. No data center operator has yet signed an agreement to purchase both the electricity and carbon removal credits from a single BECCS plant. As scope 2 accounting tightens and domestic pellet supply becomes more readily available post-2027, the conditions for structuring the first such deal are improving fast.

Pellet mills and data center developers have complementary problems: mills need offtakers, and data centers need local, dispatchable, clean power they can match to load on an hour-by-hour basis. BECCS is one of the few technologies that could solve both at once, and hyperscalers have shown they are willing to back early-stage clean firm power when the asset makes sense.

—Douglas Bryan, Senior Power and Energy Systems Modeler

Low-carbon steel: Certification frameworks are arriving

Wood-derived biocarbon has a long-established niche in steelmaking. Brazil produces roughly 10% of its steel and 30% of its pig iron using charcoal from managed eucalyptus plantations—a proof of concept for biomass as a metallurgical input, if not a direct template for US producers. The plantations measurably lowered groundwater in producer regions of Minas Gerais, and charcoal's mechanical weakness relative to fossil coke has limited the model's reach beyond Brazil.

Current pilot projects use biomass in two roles. As a fuel, industrial trials have demonstrated 10% bio-coal co-injection without operational disruption, with reviews estimating that full replacement could cut blast-furnace CO₂ by around 27% per tonne of hot metal. As a reductant, biocoke is already being demonstrated at Outokumpu's pelletizing plant in Tornio, Finland. ArcelorMittal in Belgium and Tata Steel in India are running biomass pilots at tens of thousands of tonnes per year.

What makes this market worth serious attention now is the certification landscape. The Low Emission Steel Standard issued its first certifications in September 2025. The Global Steel Climate Council's Steel Climate Standard is under stakeholder review. In May 2025, Carbon Direct and Microsoft published Criteria for High-Quality Environmental Attribute Certificates in the Concrete and Steel Sectors. These frameworks allow producers to internalize carbon price and environmental attribute certificate (EAC) values, closing the cost gap against fossil coke that has historically constrained biocarbon demand.

Carbon Direct worked with Eramet, a global metals company pursuing biogenic materials as a substitute for fossil coke at its Norwegian smelters, to assess high-quality carbon dioxide removal (CDR) methodologies and chart a path to generating and selling carbon credits from their decarbonization projects. Producers who align their sustainability credentials to these emerging standards now will be better positioned for offtake as commercial-scale demand grows.

Steelmaker pilots and the first low-carbon steel certifications are opening green-steel offtake to wood pellets, though commercial-scale demand remains limited. The producers that thrive in this market will be those that reliably deliver pellets aligned with high-quality sustainability standards.

—Louisa Brotherson, Hybrid Decarbonization Scientist

Sustainable aviation fuel: Mandates create a durable demand signal

Wood-based SAF is technically feasible via gasification to syngas, followed by Fischer-Tropsch upgrading, a proven chemistry for converting syngas to liquid hydrocarbons. Yet, the commercial challenges are substantial: the International Civil Aviation Organization estimates capital costs exceeding US$1 billion for large facilities, and production costs of US$11–48 per gallon to distillate.

The cautionary case is Fulcrum Bioenergy near Reno, Nevada, which attempted a Fischer-Tropsch process using municipal solid waste and appears to have failed due to a lack of rigorous pre-implementation testing and unrealistic timelines, a reminder that feedstock homogeneity matters enormously, and one area where pellets have a relative advantage.

Two structural dynamics make SAF worth serious attention despite those barriers. First, the European Union's (EU) SAF mandate, starting at 2% of jet fuel supply and ramping to 70% by 2050, carves out cellulosic biomass as the only qualifying feedstock once cooking oil supply is exhausted. The penalty structure in both the EU and UK creates strong demand regardless of SAF price: EU non-compliance penalties run roughly three times the price of SAF, and UK penalties can reach 13 times the cost of the fuel itself. Second, the alcohol-to-jet pathway offers a lower-capital entry point than Fischer-Tropsch, as demonstrated by Project Speedbird, a British Airways and LanzaJet collaboration targeting UK woody residues.

The near-term question is which routes have bankable offtake. Very few do yet, but the mandate structure suggests that window will shift rapidly.

So far, facilities haven't scaled to the levels required to meet timeline demand. But the EU and UK mandate structures mean buyers are greatly incentivized to purchase SAF even at high prices, rather than pay non-compliance penalties.

—John Dees, Director, Fuels and Industrial Commodities

Domestic cofiring: Achievable, but not a long-term anchor

Cofiring biomass with coal to produce electricity or heat is the most immediately achievable option. Most US coal-fired power plants could displace up to 10% of their input energy with raw or torrefied pellets, though plants would likely need fuel handling upgrades. Some state policies, such as Pennsylvania's Alternative Energy Portfolio Standards Act of 2004, support cofiring to meet renewable energy goals. However, there are no federal policies in the US that incentivize cofiring.

The case for cofiring as a long-term market is weak. The US coal fleet has contracted steadily for economic reasons—over 100 gigawatts (GW) of coal-fired capacity retired between 2015 and 2025—and biomass cofiring is unlikely to make a coal plant more cost-competitive. The Greenhouse Gas Protocol's scope 2 guidance does not permit buyers to procure a "strip" of electricity representing the biomass-fired fraction of output from a cofired plant; instead, buyers must accept the average total emissions from the plant in their scope 2 inventory, which limits the value proposition for corporate buyers seeking to demonstrate clean energy procurement.

The more interesting version of this pathway combines cofiring with carbon capture and storage (CCS), a combination that creates a deeper-abatement value proposition and the kind of firm, dispatchable power that corporate buyers increasingly need.

Cofiring is a proven step toward modest emissions reductions from coal-fired electricity, but it's hard to make the economic case for it when compared to applications that command price premiums for deeper climate abatement.

—A.J. Simon, Director of Industrial Decarbonization

Sustainability is now the qualification gate

Each of these markets is more discerning about sustainable biomass sourcing than the UK power sector was a decade ago. That shift will not reverse.

US Southeast wood has real potential for high-integrity sustainability credentials, particularly in softwood residues. But it also carries downside risks when sourcing from natural stands. Through work with producers, buyers, and project developers across these markets, we have found that four questions now drive every serious procurement conversation:

Does the supply chain have verifiable governance and chain-of-custody transparency?

Does sourcing respect the rights of Indigenous Peoples and local communities?

Is the wood coming from regions where forest carbon stocks are stable or growing, and not from protected areas or primary forest?

Is sourced biomass a by-product of non-energy uses, and not the primary silviculture driver?

Producers who can answer yes to all four, and support those answers with data, are more likely to access these emerging markets. Those who cannot will find it harder to compete for offtake.

For a detailed framework on how these principles translate into contract language and certification requirements, see the 2025 Sustainable Forest Biomass Sourcing for CDR: A Buyer's Guide.

The window is open, but not indefinitely

The US Southeast wood basket is well-positioned for the markets described here. The infrastructure is in place. What producers still need to build is the market positioning, sustainability documentation, and offtake relationships to go with it.

The producers who move now will have a meaningful head start. Those who wait for certainty may find that the most attractive offtake opportunities have already been structured around someone else's supply.

Learn more about Carbon Direct's work on SAF mandates, steel decarbonization, and sustainable biomass sourcing, or talk to our team about what this market shift means for your specific asset base.