Carbon Reduction

carbon-reduction

Carbon Accounting

carbon-accounting

Climate Strategy

climate-strategy

4 min. read

Key takeaways

Decarbonizing steel is key to meeting ambitious climate targets in the face of rapidly expanding AI infrastructure as well as broader infrastructure growth.

The gap between corporate climate ambitions and near-term commercial reality is widening. Despite strong demand signals from hyperscalers and other major buyers, leading producers have recently canceled or delayed flagship green steel projects, citing high energy costs, slow hydrogen market development, and unfavorable policy environments.

Bridging this gap requires significant capital investment and supporting mechanisms to scale low-carbon technologies. Environmental attribute certificates (EACs) offer an effective mechanism to channel capital toward transformative, low-carbon steel projects, supporting technology scale-up, as well as providing a way for buyers to meet their emissions reduction targets.

To protect the credibility of EACs as a market mechanism for decarbonization, projects should seek to meet rigorous quality criteria such as additionality, verifiability, and catalytic impact.

Forging new climate ambitions for steel production

Decarbonizing steel production is essential to meet global climate targets. Steel production accounts for approximately 7–9% of global CO2 emissions. This is driven chiefly by coal-based primary steelmaking, which still accounts for the majority of global production. Globally, at least 1.8 billion tonnes of crude steel were produced in 2025 to serve a broad array of industries including real estate, infrastructure, automotive, and data center construction.

As hyperscalers race to build the infrastructure underpinning the AI revolution, steel demand for data center construction, and associated energy infrastructure, is increasing. While the relative share of data center demand for steel versus global steel demand is small, the need for approximately 20,000 tonnes of steel per data center has a material impact on hyperscaler’s public climate commitments. Microsoft, Meta, and other large technology companies have set ambitious 2030 climate targets that include their scope 3 emissions. The embodied carbon of the steel used to build their data centers sits squarely in scope 3.

Hyperscaler’s climate commitments have generated sector-specific demand for decarbonized steel, presenting an opportunity to affect steel decarbonization more broadly. Despite this demand, the supply of low-carbon steel remains limited. The industry faces significant scale-up challenges due to the diffuse nature of demand and the nascent market. Catalyzing growth in decarbonized steel production will require market innovations and new production pathways designed to overcome these challenges. Credible environmental attribute certificates can help bridge the gap between today’s market and tomorrow’s low-carbon steel sector.

What is an environmental attribute certificate?

An environmental attribute certificate (EAC) represents the environmental attributes of a product that can be unbundled and transacted separately from the underlying physical commodity. The most widely used EACs today are renewable energy certificates (RECs), which track the environmental attributes of renewable electricity. The same concept can also be applied to steel and iron, as well as to materials such as cement and concrete.

In a book and claim model, a steel producer can implement a verified emissions reduction intervention, quantify the resulting lowered carbon intensity per tonne of steel produced, and convert that into tradeable certificates. Buyers can then purchase those certificates to support the deployment of low-carbon steelmaking capacity in cases where direct procurement of low-carbon steel is currently impractical due to geographic, contracting, or scheduling incompatibilities.

EACs are distinct from carbon credits. They do not represent emissions reduced or avoided relative to a counterfactual; they represent the intrinsic carbon intensity of the material produced, measured through a life cycle assessment.

Decarbonizing steel requires significant capital and infrastructure deployment

Steel production today

Steel is currently made via three main production routes. About 71% of the world’s steel is produced through the blast furnace–basic oxygen furnace (BF-BOF) route, which emits an average of 2.33 tonnes of carbon dioxide (tCO2) per tonne of crude steel. A further 24% is produced using scrap-based electric arc furnaces (EAFs), which emit 0.68 tCO2 per tonne on average—far lower, but still dependent on the carbon intensity of grid electricity. The remaining roughly 5% uses direct reduced iron combined with an EAF (DRI-EAF), typically using natural gas, emitting 1.37 tCO₂ per tonne on average.

While increasing scrap-based production is a critical decarbonization lever, scrap availability is limited. Primary steel production, which uses iron ore as the main feedstock rather than recycled scrap, will remain necessary at large volumes through 2050. This makes it essential to decarbonize ore-based pathways, especially ironmaking: the step where iron ore is reduced to iron and where most emissions occur.

Decarbonizing ore-based steel production requires one of three fundamental interventions: (1) replacing coal and natural gas with low-carbon fuels such as hydrogen or bio-coke, (2) electrifying ironmaking directly, or (3) capturing and storing the CO2 generated from fossil-fuel-based processes. All three involve significant capital expenditure and dependencies on infrastructure that is not yet in place at the necessary scale. As a result, the energy and cost challenge is substantial.

Low-carbon steel: emerging pathways

A range of transformative technological pathways are currently in development to overcome these barriers, offering the potential to deliver deep decarbonization to the steel industry exceeding 90% by 2050:

Hydrogen-based DRI-EAF

Using green hydrogen instead of natural gas within the DRI process provides a pathway to significantly lower the carbon intensity of ironmaking. Producers such as Stegra are deploying commercial-scale facilities designed to utilize 100% green hydrogen to reduce iron ore.

Electrifying ironmaking

Molten oxide electrolysis: Boston Metal is commercializing a process that uses electricity to directly convert iron ore to molten metal through electrolysis at high temperature, eliminating the need for hydrogen or carbon reductants entirely.

Low-temperature electrowinning: Colorado-based startup Electra uses renewable electricity to extract iron from ore via an aqueous electrochemical process that operates at near-ambient temperature.

Carbon capture and storage (CCS)

For blast furnaces and DRI plants with long remaining lifetimes, retrofitting with CCS technology can significantly reduce emissions. With new high-emitting capacity still being built, and assets expected to operate for decades, integrating CCS will be essential to avoid long-term carbon lock-in and to decarbonize these facilities over time. To date, commercial-scale deployment remains limited. The Al Reyadah facility at Emirates Steel is the only project currently capturing CO2 from a DRI process at scale, though a handful of other large-scale projects have entered the development pipeline.

Progress and setbacks: a mixed picture

The past year sent contradictory signals about the pace of steel decarbonization. On the demand side, technology companies with ambitious climate targets are actively signaling their intent to procure near-zero steel and support its development.

In September 2025, Microsoft and Stegra announced a landmark agreement that combines a physical supply deal for low-carbon steel with a separate EAC purchase agreement. Around the same time, Meta announced an agreement with Electra to purchase EACs tied to the startup’s clean iron production, becoming one of the first buyers to use the EAC model for an entirely novel, pre-commercial ironmaking technology. Nucor, the largest US steelmaker, also entered into a physical iron purchase agreement with Electra.

Despite these demand signals, the industry has experienced significant setbacks. A series of low-carbon steel project cancellations and delays has raised questions about the pace and viability of the steel transition, especially due to the high costs associated with green hydrogen production.

At present, the green premium for most low-carbon steel remains too high for buyers. A combination of sustained policy support, long-term demand signals from buyers willing to pay more, and scaling of supporting industries, such as green hydrogen production, is necessary for the low-carbon steel industry to be successful in the long run.

How EACs can bridge the funding gap in steel

EACs unbundle low-carbon steel attributes from the physical material, reducing the friction between buyers who are willing to pay a green premium and geographic or logistical constraints that may inhibit physical offtake. Buyers, such as hyperscalers procuring conventional steel for data center construction in locations where low-carbon steel is not yet available, can purchase these certificates to support the development of low-carbon capacity, attribute lower-carbon production to their steel use via a market-based mechanism, and advance toward their scope 3 targets.

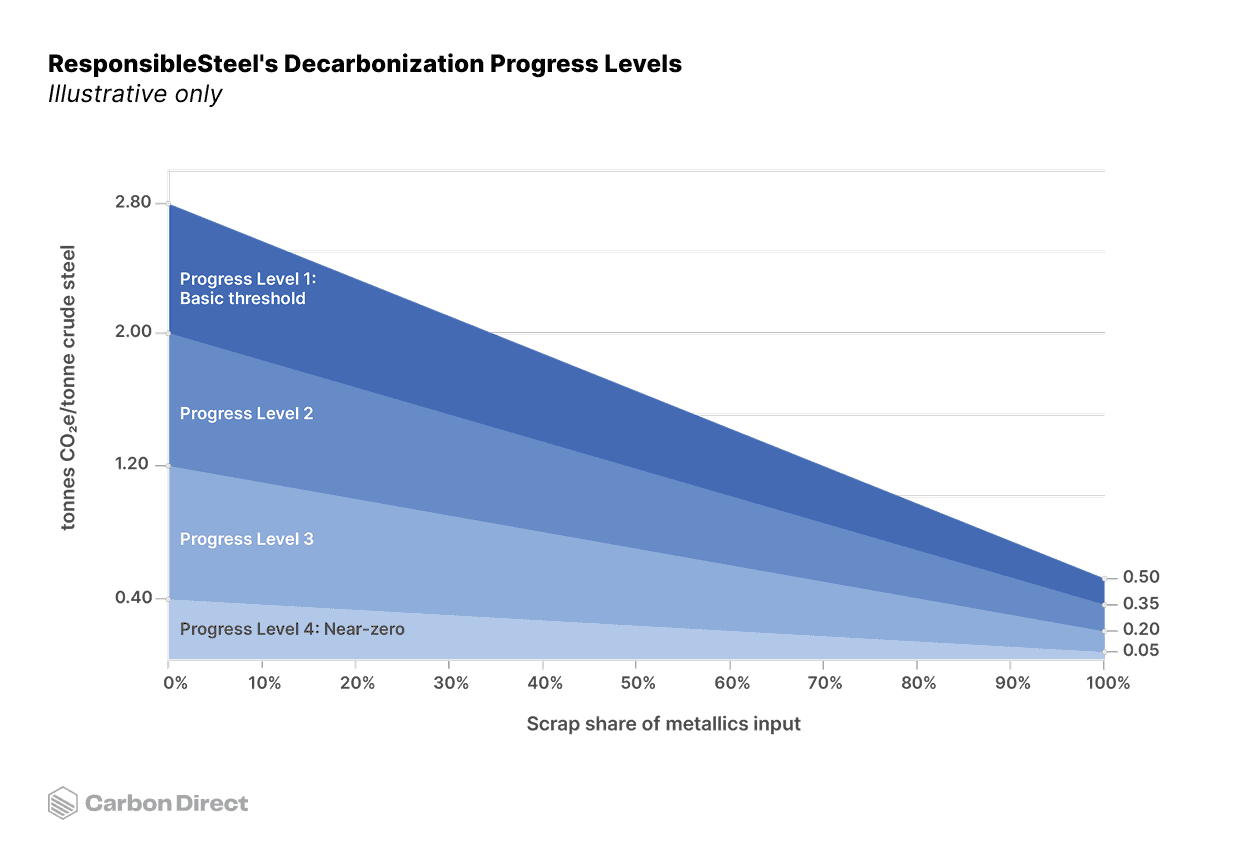

A primary objective of the Criteria for High-Quality Environmental Attribute Certificates in the Concrete and Steel Sectors, jointly developed by Carbon Direct and Microsoft, is to establish high-integrity standards for the EAC market in these sectors. For steel EACs, that means demonstrating significant emissions reduction performance by reaching at least Progress Level 2 in the ResponsibleSteel Decarbonization Progress Levels framework, and aiming to achieve Progress Level 3 by 2030. ResponsibleSteel’s scrap-variable benchmark provides a technology-neutral mechanism to evaluate emissions reduction performance by accounting for the specific proportion of scrap used.

EACs for steel are designed to be catalytic. Rather than supporting incremental improvements that are already becoming cost-competitive, they should target transformative capital changes, such as replacing BF-BOF routes with DRI-EAF, adopting low-carbon hydrogen in DRI processes, or deploying novel ironmaking technologies. Multi-year purchase agreements are particularly powerful because they provide the investment certainty that first-of-a-kind projects need to access capital at a lower cost.

What this means for buyers and suppliers of low-carbon steel

Whether you are producing or procuring steel, EACs are only one part of a broader decarbonization strategy. For buyers with significant emissions from steel, and other building materials such as cement and concrete, EACs can be a powerful tool to help advance scope 3 reduction goals where supply for physical low-carbon materials is limited. Suppliers can complement commercialization strategies for low-carbon materials by using EACs to monetize emissions reductions, generate additional revenue to support decarbonization investments, and help scale markets for low-carbon materials. Navigating the steel market requires decisions at the intersection of technical feasibility, greenhouse gas accounting, and capital strategy. Key considerations include:

Greenhouse gas accounting and reportability: Cradle-to-gate emissions for steel production must be tracked using life cycle assessments and should strive for interoperability with environmental product declarations (EPDs). EAC transactions must be reported transparently, especially given the absence of formal market standards at this stage.

Additionality and catalytic impact: EAC purchases must demonstrably support projects that would not proceed without financial support from the EAC market mechanism, and projects should have a credible pathway toward the near-zero (Progress Level 4) threshold on the ResponsibleSteel framework.

Avoiding double counting: EAC buyers must verify that the environmental attributes they purchase are not also being claimed by the physical product buyer via an EPD.

How Carbon Direct can help decarbonize steel

Decarbonizing steel is both a technical and a strategic challenge. Carbon Direct brings integrated expertise in life cycle assessment, carbon accounting, industrial engineering, and strategy to help buyers and producers navigate the complex path to decarbonization. Carbon Direct works directly with producers developing low-carbon steel technologies and with global buyers seeking credible pathways to address embodied emissions in their infrastructure, including hyperscalers working to balance climate targets with data center buildout. Our team’s expertise enables Carbon Direct to evaluate emerging EAC frameworks and ensure they deliver real climate impact.

EAC advisory for buyers: Carbon Direct helps buyers procure high-quality EACs through criteria development and in-depth technical diligence of EAC offerings across a range of low-carbon commodities, supporting purchased certificates that reflect genuine, verifiable climate impact.

EAC advisory for suppliers: Carbon Directs helps producers design high-quality EAC interventions and assess potential EAC claims throughout the supply chain, informed by technical assessment, book and claim systems, and market landscaping.

For both: Carbon Direct’s levelized cost of carbon abatement tooling provides custom modeling to assess tradeoffs across steel decarbonization pathways, helping ensure that every dollar of climate spend goes further.

Ready to move from ambition to action?

Contact us to explore how we can support your steel decarbonization strategy.