Climate Strategy

climate-strategy

Climate Policy

climate-policy

Carbon Removal

carbon-removal

Carbon Reduction

carbon-reduction

Power

power

3 min. read

Key takeaways

These topics define the climate agenda in 2025, driving urgency, influencing corporate climate strategies, and setting new expectations for action:

AI is reshaping emissions accountability. Hyperscalers are leading efforts to measure and reduce the operational and embodied carbon footprint of AI.

Carbon capture and storage (CCS) is emerging as a near-term energy solution. CCS is gaining traction as a practical way to meet rising data center power demand while supporting emissions targets.

Policy and carbon markets are accelerating climate timelines. From SBTi’s proposed carbon removal requirements to US tax incentive shifts and Japan’s GX-ETS, companies face growing pressure to act with speed and precision.

EACs are unlocking low-carbon construction. A new framework from Carbon Direct and Microsoft outlines rigorous criteria to guide credible EAC procurement for concrete and steel in data center development.

In 2025, climate action is an operational imperative

Climate action is no longer a future goal: it’s a present-tense priority. AI is redrawing emissions profiles. Policy and market developments are compressing timelines. And globally, corporate leaders face mounting pressure to act with scientific rigor, transparency, and speed.

These five topics, drawn from our most-read content in the first half of 2025, offer a window into the decisions companies are making now to operationalize climate action and lead in a rapidly shifting landscape.

Top 5 climate topics for corporate leaders in 2025

1. AI’s carbon footprint is now a business-critical issue

AI’s surging energy use has emerged as one of the most pressing sustainability concerns for corporate leaders in 2025, especially for hyperscalers.

AI’s carbon footprint has two core components:

Operational emissions from the electricity needed to run AI models. These emissions often fall under scope 2 and scope 3, making them harder to track, but increasingly material for companies scaling AI.

Embodied emissions from constructing data centers and manufacturing specialized computing hardware.

Hyperscalers are developing AI-specific emissions inventories, piloting advanced electricity emissions accounting, and investing in low-carbon building materials and energy procurement strategies. Their early moves are shaping industry expectations and influencing how other sectors approach AI’s climate footprint.

But the concern isn’t just about carbon. AI’s growing electricity demand raises questions about equity, from ratepayers facing higher bills to the impacts of data center expansion on frontline communities. In 2025, corporate leaders recognize that addressing AI’s footprint means tackling emissions and equity together.

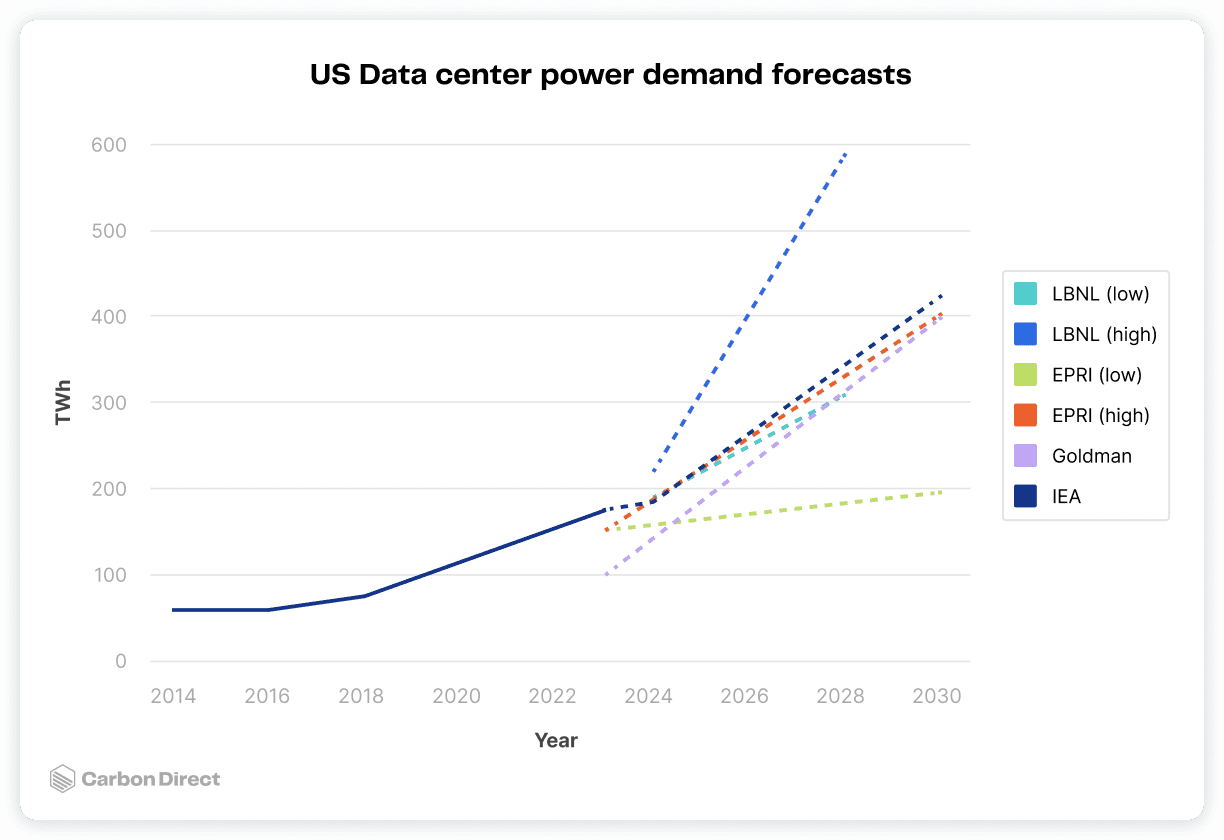

2. Carbon capture is a strategic option for powering AI

As AI accelerates electricity demand, companies are grappling with how to meet near-term needs without compromising climate goals.

Carbon capture and storage (CCS) applied to natural gas-fired power is emerging as a viable near-term solution. CCS can capture up to 95% of CO₂ emissions, and recent analysis suggests that natural gas with CCS could supply up to 63% of projected US data center electricity demand.

While long-term solutions will require a broader energy mix, CCS offers a practical bridge to support the dual goals of reliability and emissions reduction as data center infrastructure outpaces clean energy deployment.

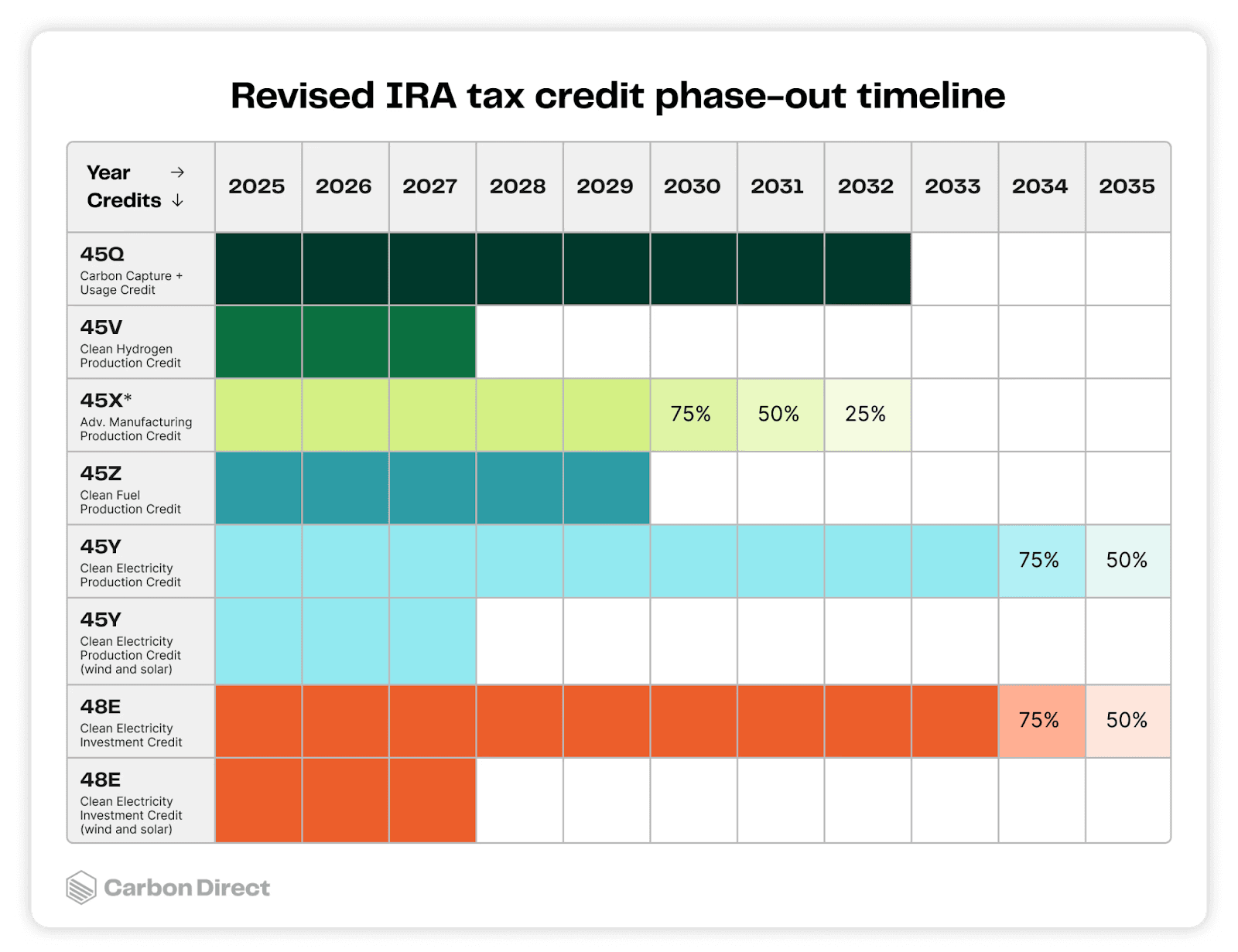

3. Policy changes accelerate near-term action

Recent policy changes in the US and globally are compressing timelines for action. In the United States, the 2025 reconciliation bill accelerates the phaseout of key clean energy tax credits, threatening the viability of future low-emissions power projects. Projects that don’t move quickly risk missing critical incentive windows, creating urgency for developers and buyers.

Globally, the Science Based Targets initiative (SBTi) has proposed revised corporate standards requiring companies to begin purchasing carbon removal before 2030 to meet net-zero targets. The draft guidance applies across scope 1, 2, and 3 emissions, raising the bar for organizations worldwide to act now on high-integrity carbon removal strategies.

Together, these changes signal a shift from long-term commitments to near-term execution.

4. Carbon markets expand and demand technical understanding

In 2025, two fast-moving developments are reshaping how companies engage with carbon markets.

Marine carbon dioxide removal (mCDR) is emerging as a priority topic for climate leaders. Once considered speculative, mCDR is now seeing early large-scale procurements, and Microsoft’s eight-figure deal in 2024 was one of the first. Interest is growing as companies prepare for hard-to-abate emissions and explore diverse carbon removal portfolios.

In response, mCDR was added as a recognized pathway in the fifth edition of the Criteria for High-Quality Carbon Dioxide Removal, published by Carbon Direct in collaboration with Microsoft. Realizing the potential of mCDR will require not only technological advancement but also robust environmental monitoring, transparent reporting, and strong alignment between project developers, buyers, and policymakers.

Japan’s GX-ETS is another hot topic in 2025 boardrooms. The market will become mandatory in FY 2026, and multinational companies with operations in Japan must begin preparing now. This includes emissions data collection, internal tracking systems, and integration with broader carbon strategies. Japan’s system is also designed for linkage with other markets, reflecting a global shift toward more enforceable, interconnected carbon pricing.

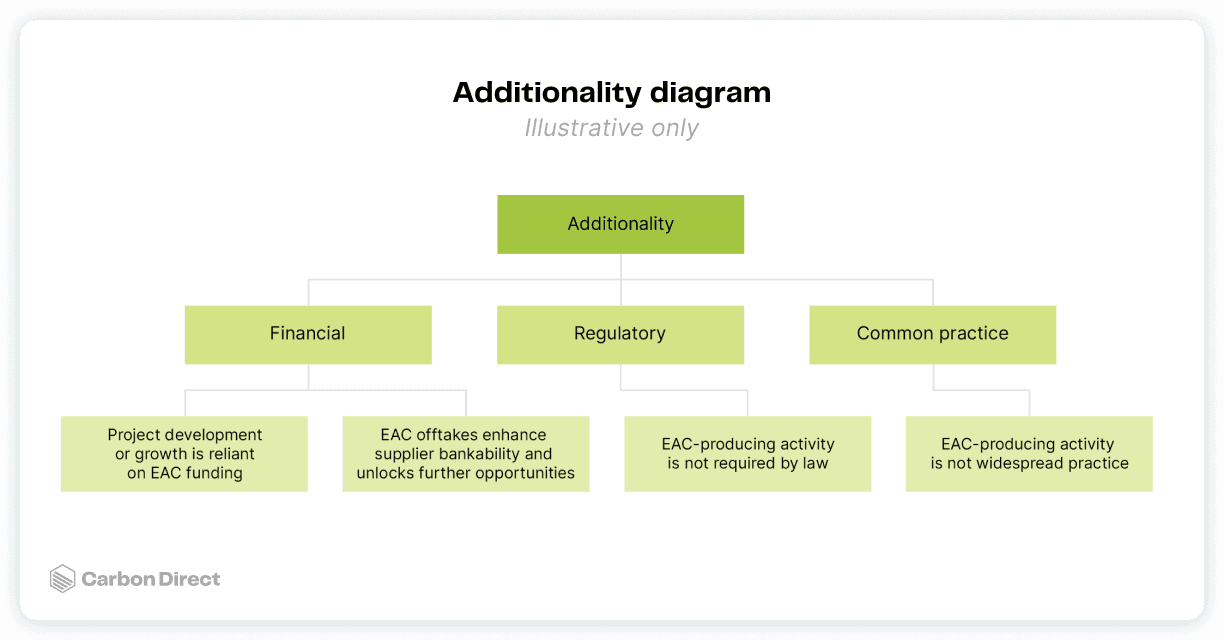

5. EACs decarbonize concrete and steel

Concrete and steel contribute 13% of global CO₂ emissions. Yet in 2025, sourcing low-carbon alternatives remains early-stage and difficult, especially for data center construction.

To address this, Carbon Direct and Microsoft developed the Criteria for High-Quality Environmental Attribute Certificates in the Concrete and Steel Sectors, the first EAC industry framework of its kind. This science-based guidance outlines seven criteria, including qualifying conditions, social and environmental harms and benefits, additionality and baselines, catalytic impact, verifiability, and leakage to support credible EAC procurement.

As demand for sustainable materials grows, this framework offers a blueprint for building a high-integrity EAC market, supporting data center decarbonization and broader climate-aligned manufacturing goals.

Why these trends matter now

From AI’s energy demands to evolving carbon markets, the pattern is clear: timelines are tightening, expectations are rising, and scientific rigor is non-negotiable.

Companies that act now, with transparency, technical confidence, and a strong climate foundation, will be positioned to lead in this next phase of decarbonization.