Carbon Removal

carbon-removal

Climate Policy

climate-policy

5 min. read

Key takeaways

Letters of Authorization (LoAs) are required when carbon credits are used within international accounting frameworks, such as the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) or compliance mechanisms tied to Nationally Determined Contribution (NDC) targets. They are not a universal mark of credit quality or legitimacy.

Currently, LoAs are rarely required for voluntary corporate climate claims. Corporate and national greenhouse gas (GHG) frameworks operate in parallel. A company claiming progress toward climate targets using carbon credits does not affect whether a host country meets its NDC—this is the principle of dual accounting.

A draft revision to the SBTi Corporate Net Zero Standard would extend corresponding adjustment requirements to voluntary carbon credits. This would reduce investment in credible carbon projects, as host countries may be unwilling or unable to authorize large volumes of CDR, meaning an LoA requirement could constrain supply below corporate demand and chill investment in high-quality projects.

The most critical question buyers and developers should ask before entering any carbon credit transaction is which accounting frameworks apply, and whether an LoA is actually required.

Letters of Authorization: Debunking a carbon market misconception

A quiet but consequential misunderstanding has been spreading through the voluntary carbon market—that any carbon credit worth purchasing must carry a Letter of Authorization (LoA) from its host country government, and without one, a credit cannot be considered credible or high-integrity. This belief, while understandable given the pace of international carbon market developments, is incorrect. If left unchallenged, it risks undermining investment in exactly the types of projects that deliver real climate impact.

The confusion stems from a conflation of distinct accounting systems: the international framework governing how countries track emissions toward their United Nations Framework Convention on Climate Change (UNFCCC) Paris Agreement commitments, and the separate frameworks by which companies track emissions toward their corporate climate targets. These systems operate in parallel, and that distinction is the key to understanding when an LoA is actually required.

What is a Letter of Authorization in carbon markets?

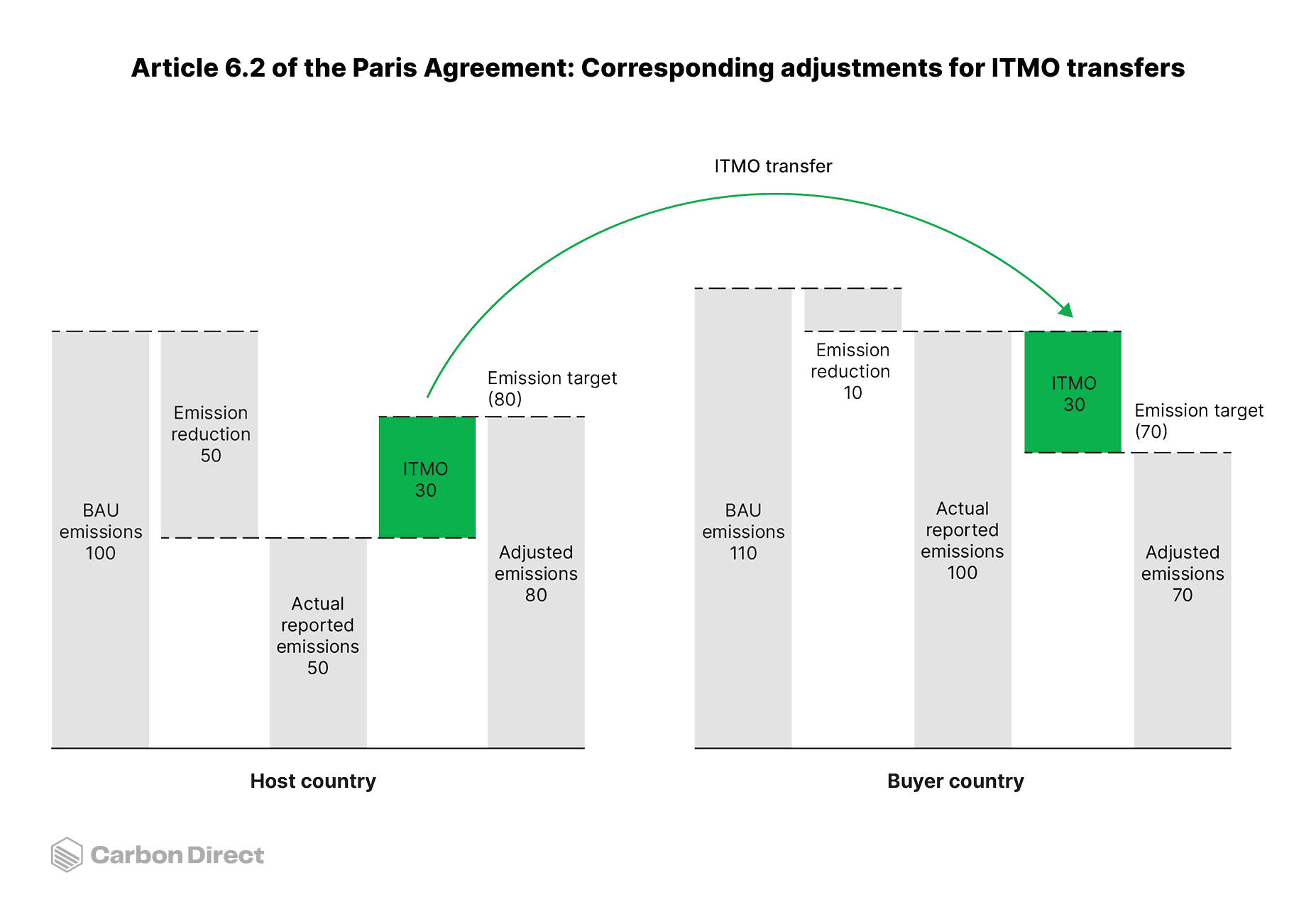

Article 6.2 of the Paris Agreement establishes rules for corresponding adjustments—an accounting mechanism that prevents more than one country from claiming credit for the same emissions reduction. When a host country transfers carbon credits to a buyer country under Article 6.2, it adds those emissions to its own greenhouse gas (GHG) inventory while the buyer country subtracts them. This ensures that each tonne of mitigation is counted only once toward national climate targets. Carbon credits that have been traded through this process are called Internationally Transferred Mitigation Outcomes, or ITMOs.

A Letter of Authorization (LoA) is the formal instrument by which a host country government confirms it will apply a corresponding adjustment.¹ It specifies the authorized uses of the ITMOs, the entities permitted to transact them, and the circumstances under which authorization could be modified or revoked. Governments typically authorize ITMOs for use toward Nationally Determined Contributions (NDCs), the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), or both.

Dual accounting vs double counting

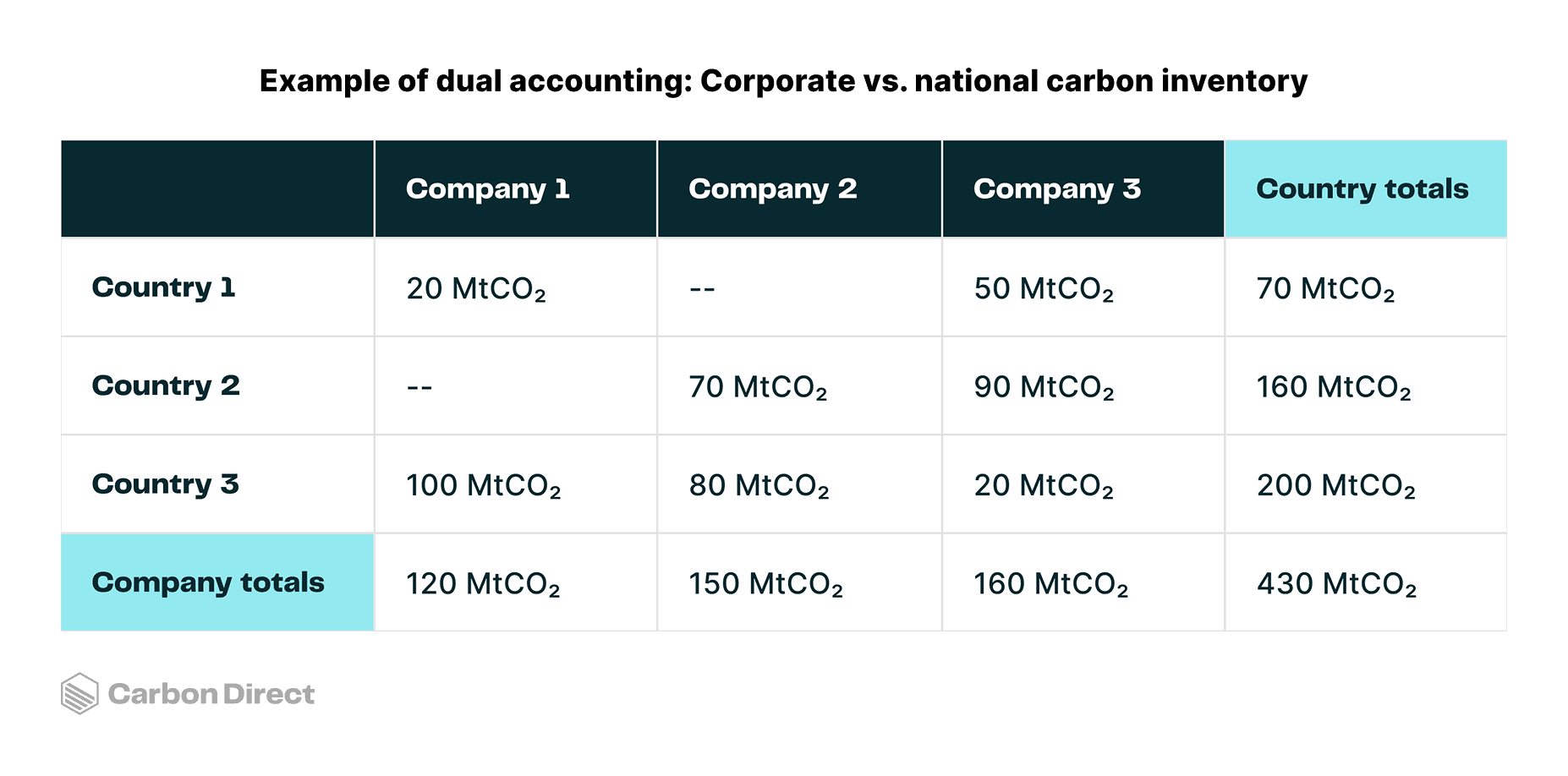

The concept that resolves this perceived tension between national and corporate inventories is dual accounting. Think of it as two parallel ledgers tracking the same physical reality. Corporate GHG inventories, governed by frameworks like the Greenhouse Gas Protocol, record the emissions and removals attributable to a given company. National GHG inventories record the emissions and removals occurring within a country’s borders.

In dual accounting, both ledgers capture the same underlying climate activity — they just do so from different vantage points. Most importantly, these ledgers are not mutually exclusive and do not enable double counting.

A 2023 analysis by Carbon Direct of the Microsoft–Ørsted bioenergy carbon capture and storage (BECCS) deal illustrates how the same carbon removal can appear in two ledgers. When Microsoft purchased carbon removal credits from Ørsted’s Kalundborg project in Denmark, those removals counted toward Microsoft’s corporate carbon accounting and toward Denmark’s national emissions inventory. Neither party was double-counting. The credits appeared in two ledgers because each is designed to capture different things: corporate accountability and national accountability.

In double counting, by contrast, a single credit is applied to two comparable inventories (e.g., by two countries) simultaneously—a practice that creates a false and inflated account of climate action.

A comparison with GDP is helpful here. National GDP and corporate revenue figures both reflect the same underlying economic activity, but they are not the same number arrived at differently—they use distinct methodologies to measure different things. GDP tracks value added across the economy, drawing on data sources well beyond company accounts, while corporate revenue figures track what individual firms earn. The two coexist without contradiction because they are answering different questions about the same reality.

Carbon accounting works the same way. Corporate GHG inventories, governed by frameworks like the GHG Protocol, record emissions and removals attributable to a given company. National GHG inventories record emissions and removals occurring within a country's borders, including from corporations, governments, and households. Again, these are separate ledgers answering separate questions, and a transaction in one does not automatically appear in the other. When a company purchases an international carbon credit, that transaction enters the corporate ledger—it does not alter what the host country or the buyer's home country reports in their national inventories.

When is a Letter of Authorization required for carbon credits?

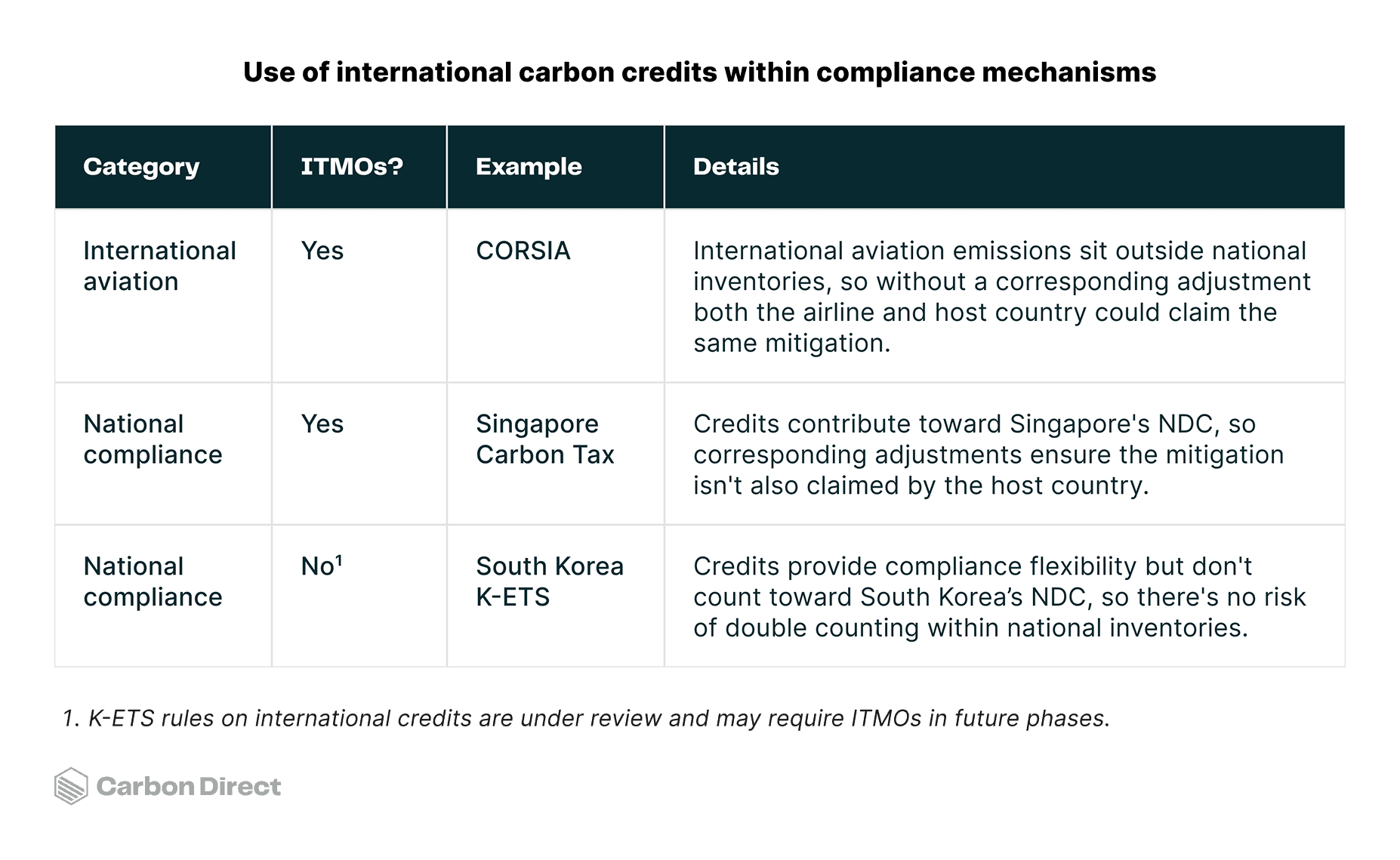

LoAs matter when a carbon credit is intended to function within the Paris Agreement carbon accounting framework. Specifically, where the same mitigation outcome could otherwise be counted more than once, either across national inventories, or between a country's national inventory and the international aviation accounting framework.

CORSIA is the most prominent example of a compliance framework requiring private companies to purchase correspondingly adjusted credits. International aviation emissions sit outside any specific country’s national inventory. However, when airlines purchase carbon credits to offset those emissions, the credits originate in countries that do have NDCs. Without a corresponding adjustment, both the airline and the host country could claim the same mitigation. CORSIA and the Paris Agreement are both UN frameworks designed to track progress toward internationally agreed climate goals—corresponding adjustments ensure the same mitigation cannot be claimed as progress in both.

A second category is regulatory compliance mechanisms that allow companies to use international carbon credits to help meet their carbon tax or emissions trading scheme (ETS) obligations. Where a scheme contributes to a country's NDC—meaning the country counts a reduction in emissions from that sector toward its Paris Agreement target—any foreign credits used must be correspondingly adjusted. This ensures the mitigation is real within the global accounting framework: the host country gives up the claim to those reductions, and the buyer country can legitimately count them.

In contrast, some compliance mechanisms allow regulated entities to retire carbon credits without those credits contributing to the country's NDC. In effect, those schemes say: you can meet a portion of your compliance obligation with carbon credits, but those credits represent investment in climate projects elsewhere, not a contribution to national emissions targets. In these cases, corresponding adjustments are not required, because the national and corporate accounting systems are not making overlapping claims.

Why LoA requirements should not extend to voluntary carbon markets

Historically, formal policies have not required LoAs for voluntary carbon credits, but that may be changing. In March 2026, Switzerland published guidance under the Unfair Competition Act requiring corresponding adjustments for international credits used towards compensation claims (e.g., carbon neutrality). Similarly, the latest draft of the SBTI Corporate Net Zero Standard v2.0 proposes the following:

“Removals used for neutralization shall not be simultaneously claimed by another entity for compliance or NDC accounting purposes. Where removals are authorized for use under Article 6 of the Paris Agreement, a corresponding adjustment by the host country shall be demonstrated. In the absence of such adjustment, the activity may only be reported as a contribution under the Ongoing Emissions Responsibility recognition framework, not as neutralization.”

This would mean that, from 2035, companies using carbon dioxide removal (CDR) credits to neutralize residual emissions toward SBTi targets would need to demonstrate corresponding adjustments.

As the SBTi standard continues to evolve, there is an opportunity to preserve the distinction between accounting frameworks that makes dual accounting work. Under Paris Agreement rules, corresponding adjustment requirements apply to international compliance frameworks—not to corporate claims made in separate accounting systems. Keeping that boundary intact would maintain a robust supply of CDR credits for voluntary action and sustain investment in high-quality climate projects worldwide. The International Emissions Trading Association (IETA) and the French Association for Negative Emissions (AFEN) have made a similar case.

If the market converges on a norm that voluntary carbon credits must carry LoAs, the consequences would be felt across the full spectrum of project-hosting countries. Developing nations are reluctant to apply corresponding adjustments that make it harder to meet their own NDCs, while wealthier countries with ambitious climate targets—where most engineered CDR projects are located—face similar barriers.

A wide-reaching LoA requirement could chill CDR investment across the board. Credits without corresponding adjustments could increasingly be perceived as lower quality or less credible—regardless of the accuracy of that perception—deterring buyers before they engage with the underlying project merits. More fundamentally, if companies cannot use CDR without LoAs toward their net-zero claims, investment in these projects will fall. The argument that a universal LoA requirement would redirect demand toward a smaller, higher-integrity supply pool depends on project host countries willing to authorize large volumes of CDR for export. Under current conditions, there are no such host countries.

Supply is already constrained. Host country governments retain full discretion over whether to issue LoAs, which project types are eligible, and on what terms. The collapse of Koko Networks in early 2026 illustrates the real-world risks of LoA dependency. The company had developed clean cookstoves credits intended for CORSIA compliance. When the Kenyan government declined to issue the anticipated LoA, the credits could not qualify for CORSIA, and anticipated buyer demand evaporated. Treating corresponding adjustments as a universal quality threshold would replicate this fragility across the broader voluntary market. At least in the CORSIA context, the case for corresponding adjustments is clear and well-founded.

Getting the accounting framework right

Understanding when LoAs are required comes down to which accounting framework is in play.

International airlines offsetting emissions under CORSIA need ITMOs because the accounting rules demand it.

For voluntary buyers, corresponding adjustments are not required for credits entering only into the corporate inventory.

Compliance buyers under national regulatory schemes fall somewhere in between, depending on how the scheme is designed.

Dual accounting is a feature of how the Paris Agreement's carbon market architecture was designed to function. Being clear about what a credit is being used for, and in which framework, is what allows both corporate climate action and national climate targets to coexist credibly.

¹ Current rules governing LoA requirements are set out in Decision 4/CMA.6, adopted at COP29 in Baku in 2024. The actual corresponding adjustments and details about ITMO transactions are reflected in Article 6.2 Initial Reports and Biennial Transparency Reports submitted to the UNFCCC.